Is there a Decline in Seed Funding?

A Startup & VC Conundrum

Money has been flowing into startups over the last decade. All around the world, innovation hubs are created, and venture capitalists (VCs) now invest globally, which is amazing!

However, different sources conclude that in the US, Europe, and Asia, even though the invested amounts may be increasing1, the number of deals is decreasing, especially at the angel/seed stage (i.e., the first financing round of a company). Here are some charts:

US: First-financing deals, flat/declining since 2015

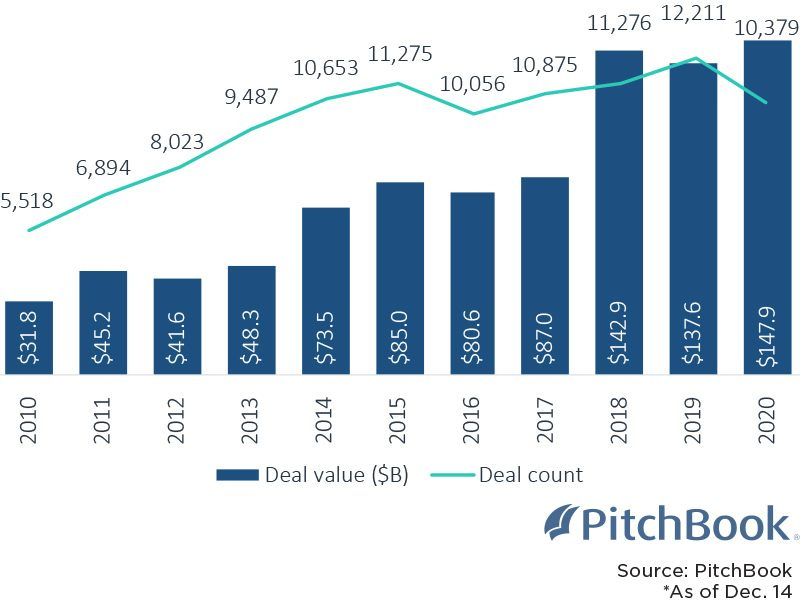

US: VC deals flat since 2015

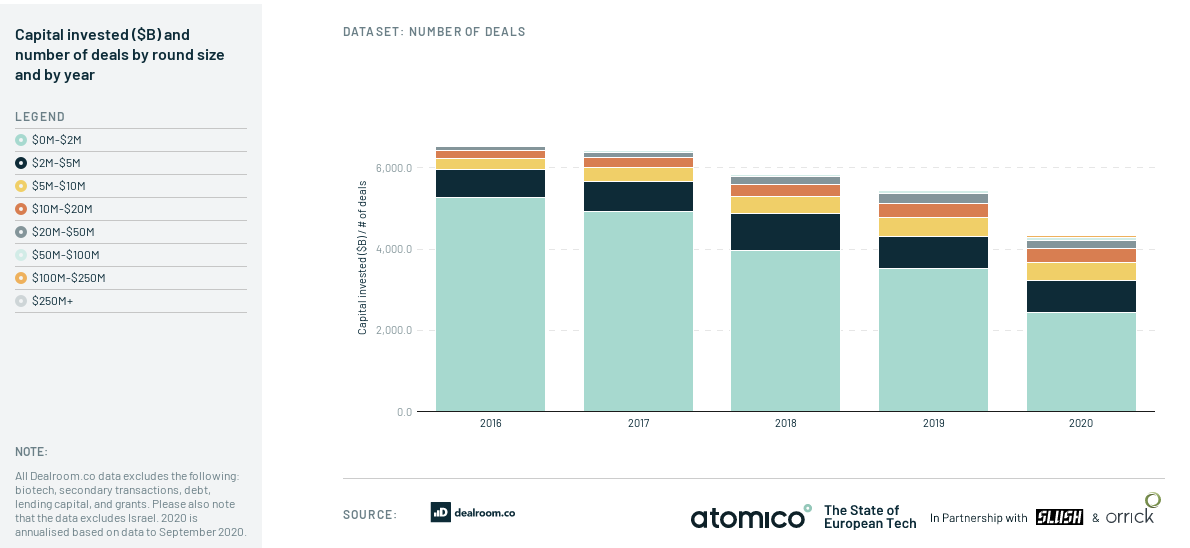

Europe: VC deals declining since 2016

Asia: VC deals, esp. angel/seed, declining since 2015

China: VC deals declining since 2016

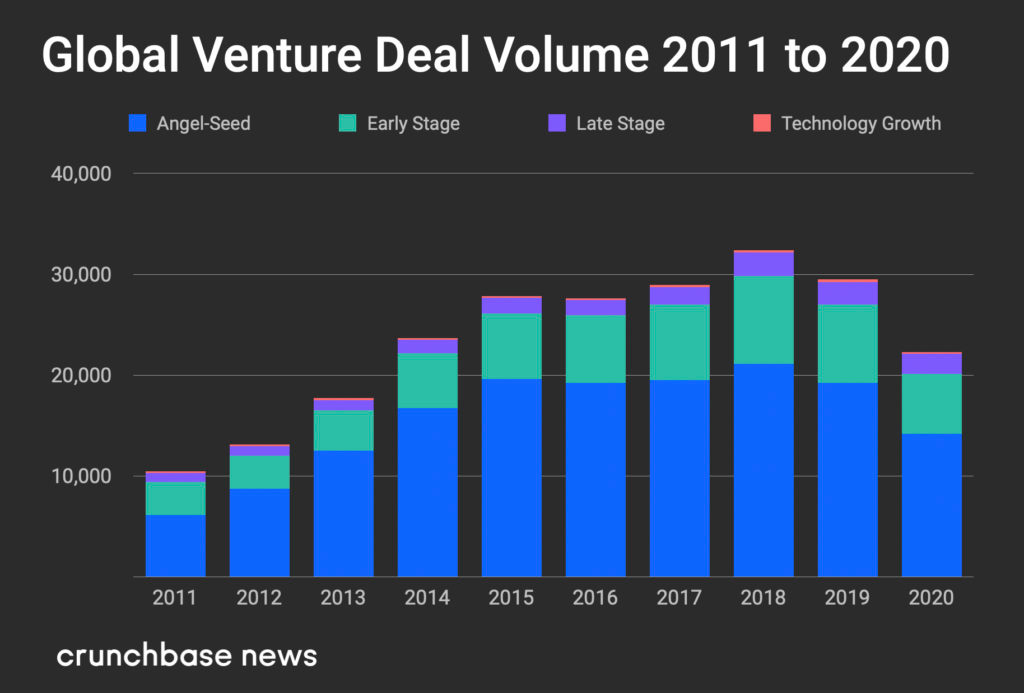

World: Angel/seed deals flat/declining since 2015

Why is the number of seed deals declining?

I don’t know! 🤷♂️

Here are some hypotheses:

Alex Wilhelm wrote in TechCrunch that SAFEs (Simple agreement for future equity) could be to blame. I’m skeptical because I don’t think SAFEs are as popular in Europe, Asia, and elsewhere as they are in the US. However, the decline is reported everywhere. And anyway, SAFEs could still be reported.

According to Crunchbase, it may just be a reporting issue: “[Seed] Funding counts trended down, but it’s worth keeping in mind that this stage of funding tends to be heavily influenced by data lags, so that number is likely to go up as more deals are added to the Crunchbase dataset over time: Often, we find as much as 40 percent of deals are added in the year after a quarter closes, and as much as 50 percent to 60 percent two years out.” But even if there were a 2-year reporting delay, data until 2018 would still be correct. And yet, the number of reported seed deals started to decline in 2015/2016.

There are maybe more and more stealth startups? However, according to Beauhurst: “the percentage share of unannounced fundraisings has remained fairly steady, fluctuating between a low of 65% in 2014 and a high of 71% in 2017 and 2018.”

Reports from PitchBook, DealRoom, Crunchbase, and Preqin may be wrong and miss many deals. Maybe, but why would they be “more wrong” today than before? Tomasz Tunguz noticed that AngelList Venture had different data, but the graph is unclear, and I don’t know if it’s the number of rounds or the round volumes in $M.

Startups may prefer alternative ways of financing, such as debt or ICO in the crypto space. And more grants are available for startups from governments or the private sector (e.g., AWS Activate).

Because it’s cheaper to start a company, and thanks to alternative financing options, many founders may bootstrap their company and later raise a proper Series A round, skipping the angel/seed step. Or they may even continue outside the VC path forever.

Some VCs may have changed their investment strategy to focus on a few big deals, especially at the later stage, rather than many small deals at the seed stage.

[Update] Some suggested on Twitter that the reports may be primarily based on press coverage. As the press coverage is limited (because the number of journalists and newspapers is limited), journalists focus on big rounds and don’t cover seed rounds. This explanation makes sense. However, the number of early-stage (Series A & B) deals has also decreased since 2018 in Asia and globally. And actually, startups don’t need the press: they can announce their fundraising on their website and social media accounts. They can even update their own Crunchbase or AngelList profile themselves to mention their fundraising. In both cases, PitchBook, DealRoom, Crunchbase, and others should be able to identify these deals and add them to their database and their report.

[Update 2] Tomasz Tunguz suggested that check sizes have increased significantly “because more capital is a strategic advantage in a market flush with money.” That makes sense, and I think that from the point of view of investors, if you have more cash to deploy, then it’s easier to do as many (or even fewer) deals with bigger rounds in each deal than to do more deals of the same size as before. This explains why the number of deals is flat/decreasing, whereas the cumulated volumes are increasing.

So two options:

If the figures are correct, maybe because of all the above factors, it means that capital is getting concentrated at the later stages (Series B+), with bigger rounds at each stage. So VCs need significantly larger exits to get a return on their investment. Also, unless fewer people start a startup, this means it’s harder to raise a seed round. But in this scenario, when you raise, you raise a lot more than before!

If the figures are wrong, then I think these reports aren’t reliable. If they don’t know the number of deals (and not even the trend), then all the conclusions drawn from them may be wrong as well.

Do you see other reasons explaining the decline? If you’re an investor, did you observe anecdotally such a decline? Or is it totally wrong? I’m curious; please let me know!

Before inflation is taken into account.

is there a correlated upward trend in series A / B funding in the past few years that would support the delayed funding hypothesis? I've noticed a few massive later rounds in the French startup ecosystem as of late but it's only a few data points